The CLARITY Act is running into a hard deadline in Washington, and the July 17 hearing in New York is more about pressure than passage. The real question is whether Congress gives U.S. crypto a durable legal framework, or keeps dragging the industry through the same regulatory swamp.

- July 17 hearing, not a vote

- Senate clock is the real bottleneck

- Bill decides SEC vs. CFTC turf

- Delay keeps uncertainty alive

The Digital Asset Market Clarity Act is not a price-pumping magic trick. It is a market structure law, the unglamorous kind of bill that can decide whether digital assets get a real legal framework or keep living under the old U.S. habit of rule by enforcement, meaning regulators mostly showed up with lawsuits instead of clear rules.

The House Financial Services Committee is holding a field hearing in New York on July 17, titled “Building the Future of Finance: How CLARITY Act Unlocks Innovation”. That hearing will not pass the bill. It can, though, force lawmakers, regulators, and industry players to say where they stand while the Senate window narrows and the August recess looms.

Why CLARITY matters

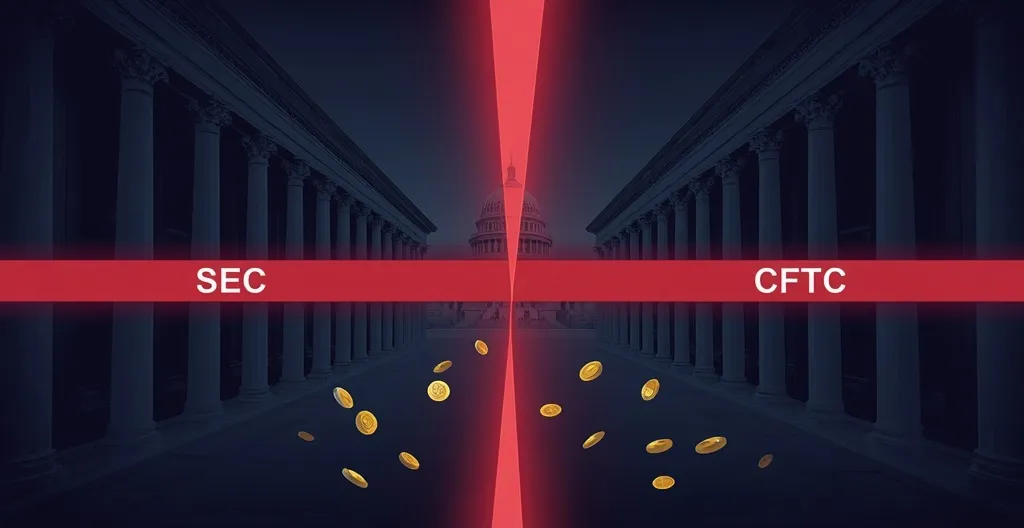

At its core, the bill is about taxonomy, the legal classification of digital assets. In plain English, Congress is trying to decide which tokens are treated as commodities and which are treated as securities.

That distinction is the whole fight. Securities fall under the SEC, which brings heavier disclosure and registration obligations. Commodities fall more naturally under the CFTC, which has a different mandate and generally less prescriptive oversight in spot markets.

That is why the U.S. crypto debate has been such a mess for years. From roughly 2017 through 2024, regulation was driven largely by enforcement actions. That can make for dramatic headlines and happy legal departments, but it is a lousy way to build a financial market. Nobody wants to spend years guessing the rules only to have them clarified by a subpoena.

That uncertainty is exactly why many institutions keep repeating some version of “statute or nothing.” They do not want a policy vibe. They want something durable.

What the Senate is staring at

The Senate returned from recess on July 13, but the bill is still waiting with no floor vote scheduled. That is the uncomfortable part. The House can hold hearings and pass legislation, but the Senate is where crypto bills go to get humbled.

Passage requires 60 votes, which means Republicans would need Democratic support. In practical terms, that means at least seven Democrats would have to come over if all Republicans stick together. That is a tough lift for any contentious bill, especially one dealing with crypto, finance, and agency turf at the same time.

The August recess matters because once Congress leaves town, floor time gets tight and political attention drifts elsewhere. The source framing that break as effectively shutting the door on contested votes for the rest of the year is a little absolute, but the basic point is right: the longer this drags, the worse the odds get.

Prediction markets are picking up that shift. Odds of passage on Polymarket reportedly fell from the low seventies to roughly 43 percent. That is a big downgrade in confidence, even if prediction markets are famously twitchy and should never be mistaken for prophecy.

What the July 17 hearing can actually change

A committee hearing cannot move a bill through the Senate. What it can do is force public positioning.

That matters because hearings can expose which lawmakers want to move, which amendments are poison, and which objections are really just cover for delay. If there are unresolved fights over DeFi, ethics language, or stablecoin yield and rewards, a hearing is where those tensions tend to surface.

In other words: it is not lawmaking fireworks, but it is still a pressure test. And in Washington, pressure tests are often the only honest things left on the schedule.

The March 17 release changed the tone, but not the endgame

A major backdrop here is the March 17, 2026 joint interpretive release from the SEC and CFTC. According to the research materials, it was a 68-page release that classified 16 digital assets as digital commodities: Bitcoin, Ethereum, Solana, XRP, Cardano, Chainlink, Avalanche, Polkadot, Hedera, Stellar, Litecoin, Dogecoin, Shiba Inu, Tezos, Bitcoin Cash, and Aptos.

That is a meaningful shift. It gives the market more clarity on how those assets are being viewed right now by the agencies that matter most.

But it is still not a statute. It is an interpretive release, which means it reflects current agency thinking rather than a permanent legal regime. A future administration or commission majority can change it. That is why the line that matters is simple: permission can expire.

For institutions, that is not good enough. They can work with guidance, but they prefer something Congress writes into law. Guidance can help a product team get to launch. A statute gives the compliance team a reason to stop sweating through its shirt.

Why institutions care so much

The CLARITY Act is not just about ideology. It affects custody, exchange listings, broker-dealer compliance, ETF product design, and whether wealth managers can allocate to crypto without living in constant gray area.

That is the boring part of the crypto revolution, and it is also the part that matters if you want serious capital to show up. Large asset managers and wirehouses do not want to build around a shifting legal target. They want clear jurisdiction, clear disclosures, and fewer surprises from regulators who decide to improvise after the fact.

The source is right to stress that a market structure bill could matter more over the long haul than any single price move. Regulation does not create a bull market by itself, but it can remove some of the legal handcuffs that keep capital on the sidelines.

The counterpoint: a bad bill can still be a bad bill

Crypto fans should not fall into the “anything that moves is bullish” trap. A sloppy law can create as many problems as it solves.

That is especially true around DeFi, or decentralized finance. DeFi refers to financial apps that run on blockchains rather than a single company’s servers. The promise is open access and fewer middlemen. The problem is obvious: if there is no central issuer, no obvious intermediary, and no neat corporate logo to subpoena, regulation gets messy fast.

That is why the treatment of protocols, developers, and front ends is such a fight. If lawmakers get it wrong, they can either smother innovation or leave loopholes big enough to drive a scam through.

Stablecoin yield and rewards is another political grenade. Banks do not exactly love the idea of stablecoin products competing with deposits. Shocking, I know. The old tollbooth class would like to keep its tollbooth. But lawmakers still have to ask whether yield products are being offered with enough transparency and whether consumers understand the risks.

There is also a narrower concern tied to Section 604 and illicit finance or trafficking. That objection deserves real scrutiny, not a wave and a smile. If critics believe a provision weakens anti-crime safeguards, they are not just being difficult for sport.

Bitcoin, Ethereum, XRP, and the market backdrop

The market itself is not exactly in euphoric mode. Bitcoin is trading near $63, 000, Ethereum is under $1, 800, XRP is holding the $1 level, and total crypto market capitalization is hovering around $2.17 trillion.

The Fear and Greed Index has spent weeks in the twenties, which is deep fear territory. So while policymakers argue over legal plumbing, the tape is still giving off the vibe of a busted neon sign in a storm.

The broader backdrop also looks hostile. The source points to inflation at a three-year high, futures markets swinging from rate cuts to the possibility of a hike, and geopolitical tension involving Iran and the Strait of Hormuz. Whether every macro piece lands exactly the same way in real time, the message is clear enough: crypto does not trade in a vacuum.

Even the best regulatory news can get run over by a nasty rates story, an oil shock, or a sharp risk-off move. Clarity helps. It does not repeal the Federal Reserve.

XRP and the institutional angle

XRP is one of the clearest examples of why market structure matters. The research notes say XRP ETFs attracted about $1.5 billion between their November 2025 launches and mid-2026. Ripple’s own materials also say U.S. spot XRP ETFs crossed $1.50 billion by early March 2026, and cite JPMorgan forecasting $4 billion to $8.4 billion in first-year inflows for XRP-related ETPs.

That is real institutional interest, not just Twitter fumes.

But it should not be oversold. ETF inflows do not equal a permanent fundamental repricing of the asset. They do show that there is demand when the legal route is clearer and the product wrapper is familiar. That is a meaningful distinction.

If Congress gives the market a more stable framework, assets already sitting in the regulatory spotlight could benefit. XRP is one of them. But turning that into guaranteed moon math is how people end up buying the top and blaming “market manipulation” when reality arrives.

Why the U.S. risks falling behind

The U.S. is not the only place writing crypto rules. The research notes point to Europe’s MiCA framework, Ripple’s authorization in Luxembourg, the United Kingdom opening its market to global crypto trading platforms this summer, and Singapore’s central bank testing settlement on public ledgers.

The exact details of every one of those comparisons matter less than the bigger point: other jurisdictions are moving toward clearer frameworks while the U.S. keeps arguing with itself.

That does not mean the U.S. is finished. It still has the deepest capital markets, the strongest liquidity, and the most important financial institutions. But capital likes predictability, and if Washington keeps dragging its feet, business goes where the rules are less stupid.

That is the uncomfortable truth for lawmakers. Delay has a cost. Overreach has a cost too. Right now the U.S. is paying both.

What happens next

There are really three paths from here.

One: the bill moves fast enough to clear the Senate before recess, which would be the cleanest outcome and the one the market would probably cheer hardest.

Two: the vote gets pulled or the bill gets stalled, which would confirm that the Senate is not ready to take the plunge. That would keep the industry in limbo and probably push a real floor fight much further out.

Three: nothing happens before recess, which may be the most Senate outcome of all. In that case, the market has to live with more uncertainty and the next serious window could slip far beyond the current political cycle.

That last outcome is the ugly one. Not because crypto needs a government blessing to exist, it doesn’t, but because modern finance runs on legal clarity. Without it, product launches slow, compliance costs rise, and capital stays cautious.

Key questions and takeaways

-

Will the July 17 hearing pass the CLARITY Act?

No. A House hearing can build pressure and force positions onto the record, but it cannot pass legislation. -

Why does CLARITY matter so much?

It could decide whether digital assets are regulated as commodities or securities, which determines whether the CFTC or SEC has primary oversight. -

Why isn’t the March 17 SEC/CFTC release enough?

Because it is an interpretive release, not a statute. It helps, but future agency leadership can change it. -

What is the biggest obstacle in the Senate?

The bill needs 60 votes, so Republicans need Democratic support. The calendar is tight, and August recess makes a floor fight harder. -

Can macro still crush crypto if the bill advances?

Yes. Rates, inflation, oil shocks, and geopolitical stress can overpower regulatory optimism in the short term. -

Why do institutions keep asking for a statute?

Because they need durable rules for custody, compliance, listings, and product design. Guidance helps, but law lasts longer.

The CLARITY Act is the kind of bill that could shape the next phase of U.S. crypto adoption without doing much to prices on day one. That may disappoint traders hunting for instant fireworks, but it is how structural change usually works: slowly, through committees, amendments, and enough political friction to grind the air out of the room.

If the Senate moves, the industry gets closer to a real framework. If it stalls, the U.S. keeps exporting uncertainty while other jurisdictions keep writing the rules. That is bad for builders, bad for institutions, and bad for anyone tired of watching America turn basic policy into a cage match.

This article is information, not investment advice.

Further reading

For the legal and institutional backdrop around crypto market structure, these resources add useful context.

- Oversight of the Federal Home Loan Bank System

- The SEC's Crypto Commodity Framework: What Digital Asset Professionals Should Watch

- XRP's Institutional Breakthrough: From Courtroom to ETF

- 119th Congress (2025-2026): Digital Asset Market Clarity Act Text

- Clarifying the CLARITY Act: What to Know

- CLARITY Act: Senate Banking Releases New Text and Markup Analysis

- CLARITY Act Advances as U.S. Crypto Market Structure Fight Intensifies

- Senate Banking Committee Advances CLARITY Act to Split Crypto Oversight Between SEC and CFTC